test prep strategy

In a Recession, Test Prep Is the Spend Families Don’t Cut

By the spring of 2026, parents did not need to go looking for economic anxiety. It arrived uninvited in push alerts, market headlines, grocery totals, tuition conversations, and the uneasy language of experts trying to name what might come next.

Tariffs. Trade wars. Inflation. Recession risk. Volatility.

The words blurred together, but the feeling underneath them was familiar enough: the sense that the household math might soon have to change.

In a recent NerdWallet survey conducted by The Harris Poll, 65 percent of Americans said they believed the U.S. economy would enter a recession within the next twelve months. Goldman Sachs raised its 12-month U.S. recession probability to 30 percent in March. Furthermore, according to the New York Fed, total U.S. household debt reached a record $18.8 trillion in the first quarter of 2026.

It is in this kind of climate that the question begins to arrive at our office.

Sometimes those concerns are spoken aloud in consultations. More often, it is implied in the careful way parents weigh what to renew, what to delay, and what to pause.

Is this still worth it right now? It is a fair question.

What We’re Seeing

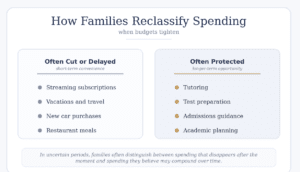

“The families who understand what’s at stake don’t pull back,” Clayborne CEO Lee Elberson said during a recent interview with Cville Right Now. “What we see is actually a sharpening of priorities. People cut streaming services and vacations first. Education, especially college admissions support, sits at the very bottom of the cut list. What changes in uncertain times is that parents become more intentional about the spending they keep, not less.”

What we have seen, in truth, is more layered than a single pattern.

The first half of this year was, by industry consensus, harder than the same months in recent memory. Sign-ups slowed across the test prep landscape. In conversations Clayborne Education has had with other test prep companies, the same observation kept returning: everyone was feeling the cuts by the spring, but families were not necessarily abandoning test prep all together, they were waiting.

The decision was not to walk away from preparation. It was to kick the can down the road, pushing off the conversation sometimes by weeks, sometimes by months.

In recent weeks, we have watched some of that deferred spending return. Summer sign-ups have begun to gather pace again. Parents who paused in February have come back in May with the same questions, often more decided: What will tutoring actually move? What will it not be? Does beginning in May rather than August make a meaningful difference? What kind of return should we realistically expect?

These are good questions. They are the kind of questions careful parents ask in uncertain times. They are also the kind of questions parents asked during the last hard year, and the kind parents asked our predecessors during the recession before that.

The pattern is older than any of us in this work.

The Pattern Across Downturns

Education spending behaves differently from other categories. Not always, not for every family, and not without strain. But historically, when the economy tightens, families do not stop caring about academic preparation. If anything, they begin to scrutinize it more closely.

A streaming subscription is a want. A vacation is a discretionary expense. A new car can wait. A restaurant meal can become dinner at home.

But tutoring, for the families who choose it, occupies a different mental category. It belongs to the class of expenses parents understand as compounding: the kind of investment whose value may not be visible in the moment, but may matter deeply later.

This is not a new instinct. During the Great Recession, college enrollment rose rather than fell, with the sharpest increase at two-year colleges. The U.S. Census Bureau later reported that enrollment at two-year colleges increased by 33 percent from 2006 to 2011.

The logic was straightforward, and many parents who lived through that period remember it well: when the job market is harder, credentials matter more.

When the future feels less stable, families look more carefully at the investments that might widen a child’s options. Economists call this human capital allocation. Most parents simply call it the thing you don’t cut.

The Numbers, Honestly

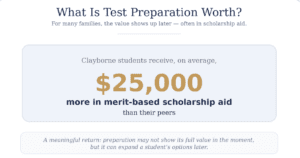

A reasonable person, reading all this, might want to see the math.

Clayborne students receive, on average, approximately $25,000 more in merit-based scholarship aid than their peers. That is a meaningful number, and it is the one we point parents toward most often when they ask, with all due seriousness: What is this actually worth?

A useful way to think about the answer is the way a CFO thinks about a budget line.

Some spending is consumption: it brings enjoyment, convenience, or short-term relief, but no expected financial return. Other spending is investment: it is meant to produce future value.

Tutoring, when used well, belongs much closer to the second category. A modest annual investment in test preparation may return several multiples of itself in scholarship dollars across four years of college. It may also help a student approach the admissions process with greater confidence, more options, and a clearer sense of what is possible.

That does not mean every student needs the same plan. It does not mean every family should make the same investment. It does not mean tutoring is magic, or that test preparation can substitute for years of academic work.

But it does mean the question should not be framed only as: Can we spend this right now?

The better question is: What might this return?

And that is one of the reasons that, when families come to us during economically uncertain times, they often come with sharper questions. They want to understand the return. They are skeptical in the productive way that parents under financial pressure tend to be. They are not looking for excess. They are looking for leverage.

That is exactly the right instinct.

What Recently Changed

There is another reason the conversation looks different this year.

Under expanded federal 529 rules, families may now use 529 funds for a broader range of K–12 expenses, including tutoring, standardized test fees, curriculum materials, and online educational tools. Beginning in 2026, the annual K–12 withdrawal limit rises from $10,000 to $20,000 per student. Families should still check their own plan rules and state tax treatment before making withdrawals. For families who already have 529 funds set aside, this matters.

Read our full breakdown of how 529 funds could pay for test prep.

Preparation that once had to be paid for from after-tax income may now be funded through money already designated for education. A family weighing whether to begin or continue test preparation under tighter conditions is therefore not looking at quite the same equation. A tutoring investment financed from a 529, especially when paired with the possibility of merit scholarship aid, looks meaningfully different on a family balance sheet than the same number pulled from a checking account already under strain.

We wrote about this development when the bill passed last summer. It is even more relevant now than it was then.

The Wider Story

It would be dishonest to write about education spending and economic uncertainty without acknowledging the obvious: strain is not distributed evenly.

Some American households continue to spend roughly as they always have. Others are tightening significantly. The gap between those two realities is widening.

We are aware of which families that gap protects and which families it strains. We are also aware that the students most likely to benefit from rigorous preparation are not always the students with the greatest financial cushion behind them.

For those families, the case for planning carefully is not weaker. It is stronger.

That may mean using a 529 strategically. It may mean starting with a diagnostic before committing to a larger package. It may mean choosing the highest-impact work first: a test selection conversation, a focused section score plan, a study schedule, or a few months of consistent preparation rather than a last-minute scramble.

The point is not to spend for the sake of spending. The point is to make the spending count.

The reason many wealthy families continue to invest in education through downturns is not only that they have spare cash. It is that they understand the math. They understand that academic preparation, done well, can affect options later.

That logic should not belong only to families with the largest cushion.

Recommendations

When Elberson was asked what a parent of a current ninth grader should do if they were hearing this conversation for the first time.

Start with a diagnostic.

Understand where your student actually stands before making larger decisions. What are their strengths? Where are the gaps? Which test is the better fit? What kind of timeline is realistic? What support would actually matter?

The most expensive mistake families make in tutoring is often the same mistake investors make in markets: trying to time the move perfectly rather than starting with good information.

Time in the preparation, not timing the preparation, is what compounds.

For families in Central Virginia thinking about this for the first time — or thinking about it again, more carefully than they did six months ago — a single diagnostic is the conservative version of getting started. It does not require a sweeping commitment. It gives families a clearer picture of where their student stands and what kind of preparation would be useful.

In uncertain times, clarity has value.

Listen to Elberson’s full conversation on Cville Right Now with Alex Hawes.

Share this: