For more on this story, listen to Lee on the radio:

School just let out, and a lot of parents are standing at the same fork in the road: Do I keep my kid in academic mode all summer, or do I let them completely check out?

It’s a fair question but I’d gently push back on the question itself. More-school versus no-school misses the most valuable thing summer can actually do. School delivers content, on a schedule, to a group, on a clock. Summer is the rare stretch where a kid has time, autonomy, and low stakes all at once. That combination builds the skills that never show up on a report card.

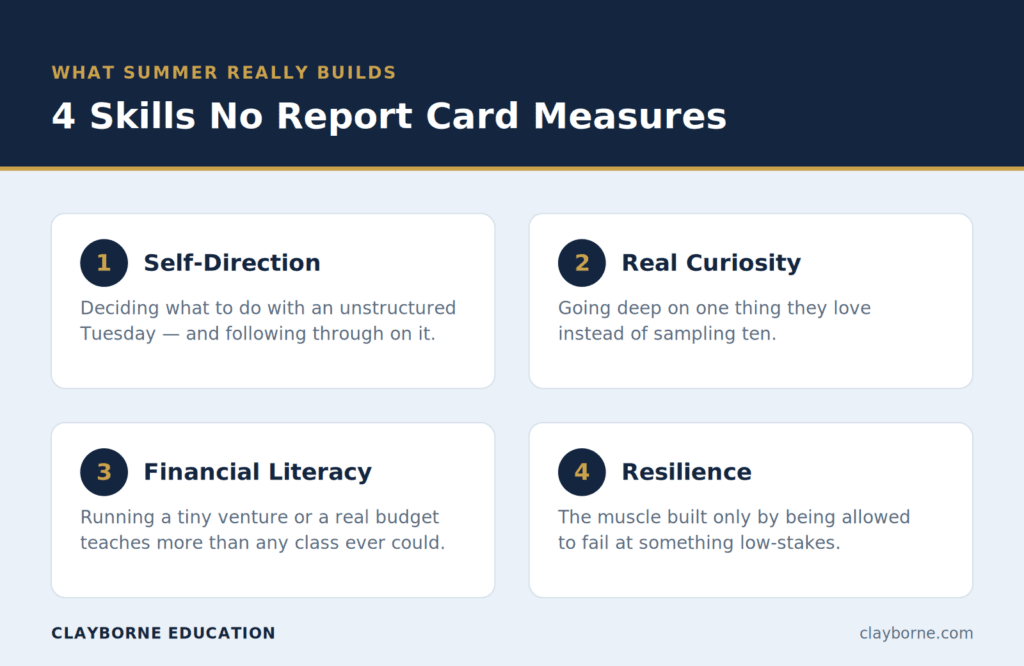

When parents ask me to get specific, I point to four. They sound “soft,” but they’re the ones that actually carry a young person, and in an uncertain economy, they matter more than one more worksheet packet, not less.

Self-direction is figuring out what to do with an unstructured Tuesday. And more explicitly, sticking with something hard because you chose it, not because it’s graded. Real curiosity means going deep on one thing instead of sampling ten, and it matters more than parents tend to think: a widely cited meta-analysis of roughly 200 studies found that intellectual curiosity is a “third pillar” of academic achievement, with an effect that rivals conscientiousness. Financial literacy is something schools barely touch. A teenager who runs a tiny summer venture, or just manages a real budget, learns more about money than any class delivers. And resilience is the muscle you only build by being allowed to fail at something low-stakes and recover.

How do you encourage that without turning summer into one more packed calendar? Mostly by stepping back. The goal isn’t to schedule these skills; it’s to leave enough room that they can emerge.

When the future feels less certain, the temptation is to double down on credentials and test scores. Because those do matter and we’ll get to them. But what truly makes a young person adaptable when the ground shifts isn’t another line on a transcript. It’s the initiative and resourcefulness underneath it. Think of it the way a CFO reads a balance sheet: content is consumption, but these durable skills are the investment that compounds.

Building that intentionally does take some support — and yes, some spending. Which is exactly the conversation every family I talk to is having right now.

Why families are weighing every education dollar more carefully this year.

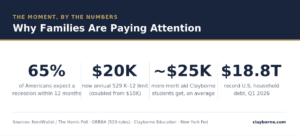

The anxiety is real and measurable. About 65% of Americans told a NerdWallet survey (conducted by The Harris Poll) they expect a recession within twelve months, and total U.S. household debt sits at a record $18.8 trillion, according to the New York Fed. Parents feel it acutely: in one recent NerdWallet index, nearly half of parents with children under 18 said they expected to lean on credit to get through the month. We unpacked how families actually respond to that pressure in In a Recession, Test Prep Is the Spend Families Don’t Cut — the short version is that education tends to be the last line they cut, not the first.

What actually changed this year: the 529 rules

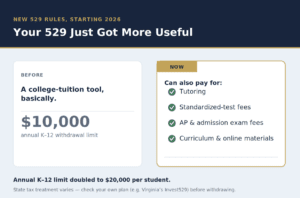

Here’s the piece most families haven’t caught up to. A 529 used to be a college-tuition tool, basically. Under the new federal rules in the One Big Beautiful Bill Act, two things changed at once. First, the amount families can pull for K–12 expenses each year doubled — from $10,000 to $20,000 per student, starting in 2026. Second, and bigger for us, the list of what qualifies expanded to include tutoring, standardized-test fees, AP and college-admission exam fees, and curriculum and online materials.

Preparation that used to come out of the checking account can now come from money already set aside for education.

That changes the math on a family’s balance sheet. A tutoring investment financed from a 529 — paired with the merit-scholarship aid that good preparation can unlock — looks very different from the same number pulled from a checking account that’s already under strain. (We walk through the full mechanics in how 529 funds can now pay for test prep.)

There’s now a tax-advantaged way to fund preparation that didn’t exist eighteen months ago.

Before you withdraw

These expenses are qualified at the federal level, but state tax treatment can differ — Virginia families using Invest529 should check their own plan rules first. The annual cap also covers all those categories together (tuition plus tutoring plus books can’t exceed the limit). When in doubt, talk to whoever does your taxes. This isn’t tax advice — it’s a heads-up that a useful option now exists.

The squeeze is happening at school, too

This isn’t just playing out at kitchen tables — our own school divisions are navigating tight budgets. Albemarle just adopted its 2026–27 budget, and both county and city divisions spent the past year managing real uncertainty over federal title-grant money. Last summer there was a scare where Albemarle was looking at roughly $660,000 and Charlottesville around $417,000 in exposure before it was resolved.

When public schools are stretched, support services are usually where the strain shows up first: fewer counselors, larger classes, less individual attention. That’s exactly the gap families end up looking to fill from outside — a double squeeze, where the need for support tends to rise precisely when families feel least able to pay for it.

Who gets left behind

Let’s be honest about something: not every family is feeling this the same way. Some households are spending roughly as they always have. Others are tightening hard, and that gap is widening. Here’s the uncomfortable part — the students most likely to benefit from rigorous preparation aren’t always the ones with the biggest financial cushion. For those families, the case for planning carefully isn’t weaker. It’s stronger.

So what does “planning carefully” look like when the budget is genuinely tight? It means making the spending count instead of spending for its own sake: use a 529 strategically if you have one, start with a single diagnostic before committing to a big package, and do the highest-impact work first — a test-selection conversation, a focused plan for the sections that move the score, and a realistic testing timeline — rather than a last-minute scramble in senior fall.

The reason wealthy families keep investing through downturns isn’t only spare cash. It’s that they understand the math. That math shouldn’t belong only to them.

That conviction is a big part of why we run a Community Access Program at Clayborne.

The one move to make this week

If you’re a parent of a current ninth grader hearing all of this for the first time, start with a diagnostic. Understand where your student actually stands — strengths, gaps, which test fits, what timeline is realistic — before you make any bigger decision. The most expensive mistake families make is the same one investors make: trying to time the move perfectly instead of starting with good information.

It’s time in the preparation, not timing the preparation, that compounds.

In uncertain times, clarity itself has value — and a single diagnostic is the low-commitment way to get it.

Start with clarity, not a big commitment

Lee Elberson is the CEO of Clayborne Education, a test-prep and academic-tutoring company that works with families in Charlottesville, Richmond, Chicago, and remotely nationwide. He spoke about these trends on the Adam Hawes Show; you can listen to the full segment here.

Share this: